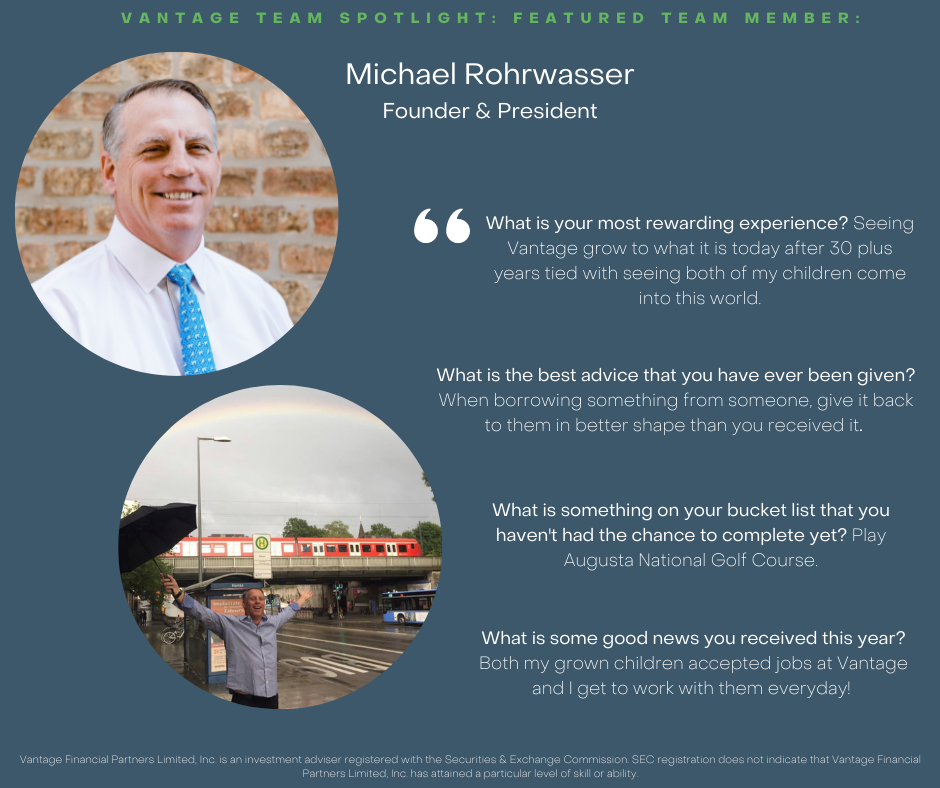

Michael Rohrwasser is the President and Founder of Vantage Financial and we are excited to be spotlighting him. To learn even more about Michael, visit is his bio here!

The articles below offer general information, opinions, and forecasts and should not be considered advice.

Michael Rohrwasser is the President and Founder of Vantage Financial and we are excited to be spotlighting him. To learn even more about Michael, visit is his bio here!

Market Memo

December 2021 – Dan Zalipski, CFA®

The last several weeks have been volatile with a series of headlines moving the markets. The day after Thanksgiving, while many Americans were out shopping for the holidays, word of the new COVID variant Omicron was announced. Carrying more mutations and being more transmissible than the Delta variant, the Omicron variant was flagged as being able to potentially evade protection from the current lineup of COVID vaccines, sending the market lower while the world waited for more data. Fortunately, it appears that the current vaccines and antiviral medications will help reduce the worst-case scenarios, but an increase in break-thru infections is possible. Investors expect consumers will curb their behavior in the weeks ahead in response to Omicron. Restaurants are already beginning to see a decline in patrons, and numerous professional sporting events have already been postponed. Similar to the Delta wave, consumers will likely reduce their activity regardless of what the government suggests.

Continue readingDecember 2021 – By Bob Veres

Anecdotally, we hear that anybody who wants to find a job today will find him/herself in a competitive bidding situation. There are articles that advise job seekers on how to manage competing salary offers, while articles for employers offer advice on how to avert bidding wars for valuable members of their staff. Other articles simply say to current workers that this is a good time to ask for a raise.

Continue reading

Here at Vantage, we believe in Investing in Kindness. We talk a lot about serving our clients and serving each other, but we want to take our company values of integrity and teamwork beyond that and ask ourselves, how else can we give back? Our team took the afternoon off on Tuesday, November 30th to volunteer our time at Feed my Starving Children to pack meals for kids living in poverty around the world. Our shift accomplished boxing 27,432 package meals and fed 75 kids for a year! We had so much fun throughout the packing process and felt grateful to have the opportunity to give back as a team!