March 2025

The Social Security Fairness Act is a bill signed into law that repeals several decades-old provisions that previously reduced your Social Security benefits if you or a spouse received a pension from a non-Social Security covered job, and now restores these benefits, allowing you to receive the full Social Security retirement benefits earned based on individual work histories. In this article, we will discuss Social Security and how the changes may impact you and your financial outlook and ensure your strategies align with your financial goals.

What are the basics of Social Security?

Social Security benefits were created as a way to replace some of your earnings when you retire or have a disabling condition preventing you from continuing to work. Your benefit payment is calculated based on how much you earned during your working career. The more you earned over your working life the higher the benefits and if there were years you didn’t work or experienced lower earnings, your benefit amount could be lower than had you been steadily employed.

Does it matter when I choose to receive retirement benefits?

At what age you decide to start receiving your retirement benefits from Social Security in part determines how much you will get. If you opt to start getting them when you reach full retirement age, you’ll receive your full benefit. Your benefit could be reduced if you begin receiving the benefits before you reach full retirement age. If you choose to continue working beyond full retirement age your benefit could increase.

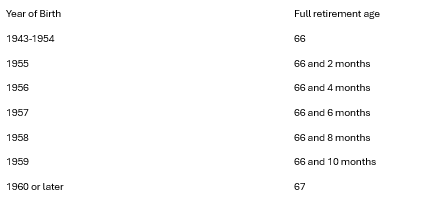

What determines full retirement age?

In 2025, if you were born in 1957 or earlier, you are eligible for full Social Security retirement benefits. According to the Social Security Administration, full retirement age is based on the following information:

What if I collect retirement benefits before full retirement age?

It is possible to receive benefits as early as age 62, however, if you choose to start early, your benefit amount will be reduced by about 0.5% on average for each month you begin accepting benefits before your full retirement age. Essentially, if your full retirement age is 67, and you sign up to receive benefits at age 62, you would only receive about 70% of the full benefit.

What if I wait to retire until after full retirement age?

If you wait until after full retirement age to receive benefits the Social Security Administration will increase your benefit by a specified percentage depending on the year you were born. Each month you delay receiving benefits after hitting full retirement age, the amount you will receive will increase automatically, monthly, until you start receiving benefits or reach age 70, whichever comes first.

Can I receive benefits and continue working?

You can receive Social Security benefits while you are still working, however, as mentioned, if you are younger than full retirement age, your benefits could be reduced if you earn more than a certain amount.

I heard the Social Security Fairness Act got rid of penalties. Is that true?

Yes, that is true. The Social Security Fairness Act eliminates penalties known as the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO), two rules that lowered payments to certain retirees who receive pension income. Now, with the changes to the legislation, those individuals who had paid into Social Security can potentially receive the full benefits that were previously limited or even eliminated.

Originally, they looked at the pension the workers were going to receive and the social security check they were going to receive, and they would place a penalty based on a combination of things. According to congress.gov, the Windfall Elimination Program (WEP), in some cases lowered Social Security benefits for individuals who also received a pension or disability from an employer that didn’t withhold Social Security taxes. The Government Pension Offset (GPO), in some cases, lowered Social Security benefits for spouses, widows, and widowers who simultaneously receive a government pension. Now that is gone.

According to the recently passed legislation, public-sector workers, spouses, and survivors (widows and widowers) affected by the WEP/GPO can expect to receive an average increase of around $360 per month in their Social Security benefits , with certain workers noticing increases of up to $587 per month depending on their situation. Some individuals may also receive a lump sum payment for funds they are owed.

What can workers expect is going to happen next?

The Social Security Administration is developing new processes for computing retroactive benefits and processing new and pending claims.

Will every public worker, police officer, teacher, and firefighter be eligible for benefits because of the passing of the Social Security Fairness Act?

Despite some articles indicating otherwise, not every public worker will be necessarily eligible. Only those who receive a pension based on work not covered by Social Security could receive benefits. A financial professional can help you determine if you are eligible and how the new law may impact your financial situation and strategy.

What is the foundation for the changes?

Most jobs are covered by Social Security, which translates into a 6.2% tax withholding for the employee. And that tax is matched by a 6.2% employer payroll tax contribution. Maximum income subject to tax is capped at $176,100 in 2025. However, many public sector workers are employed in state and local government jobs that Social Security doesn’t cover. Instead, they have been eligible for a pension. While Social Security doesn’t cover their government jobs, some workers may have held other jobs in the past or alongside their current jobs that allow them to pay into Social Security and be eligible for those benefits.

The provisions were originally meant to prevent certain beneficiaries from receiving higher Social Security benefits than they earned. Critics claimed they led to unfair reductions for some people. Therefore, the provisions were eliminated after many years of political red tape.

The Social Security Fairness Act as it applies to benefits for spouses and surviving spouses

Individuals receiving surviving spouse benefits can be quite complicated. You can switch to your own benefits as early as age 62 assuming your retirement benefit is more than the amount you receive on your deceased spouse’s earnings. In some cases, if eligible, you can receive one benefit at a reduced rate and switch to the other benefit at the full rate when you reach full retirement age.

The Social Security Fairness Act as it applies to benefits for people with disabilities

As briefly mentioned earlier, the Windfall Elimination Provision (WEP) reduced Social Security disability benefits for those who received a pension from a job where Social Security taxes were not withheld. The Social Security Fairness Act eliminates that provision so people with disabilities who receive such pensions will now receive full disability benefits without them being reduced.

You may be eligible for Social Security disability benefits if you can’t work because of a mental or physical condition that has lasted or is expected to last at least 1 year or results in death. Be aware that just because you are eligible for disability from another government agency or a private plan, doesn’t mean you will automatically be eligible for Social Security benefits. Their criteria are different. You can apply for Social Security disability benefits at www.ssa.gov/disability.

The Social Security Fairness Act as it applies to benefits for divorcees

The changes to the legislation significantly benefit divorced individuals as the elimination of the WEP and GPO provisions previously reduced Social Security benefits for divorced spouses who also received pensions from non-Social Security-covered jobs preventing them from receiving a higher spouse benefit from their ex-spouse based on their full work record. That no longer applies.

How can you apply for benefits?

If you previously filed for Social Security benefits and they are partially or completely offset, you don’t have to take any action aside from verifying that the SSA has your current mailing address and direct deposit information. This can be done online through the “my Social Security account” here: www.ssa.gov/myaccount

If you are receiving a public pension and are interested in filing for benefits, you can file online at www.ssa.gov/apply or schedule an appointment to speak with a representative.

Are you owed anything?

The Social Security Administration website, www.ssa.gov houses your account where you can preview your statements by accessing them through the Social Security website. You sign in and then can see your actual benefits to date. You can review both statements and the section that lists earnings by year as the statements group them.

Are statements accurate? I have heard they aren’t.

Statements weren’t necessarily accurate in the past because penalties used to impact the amount totals. That is no longer the case. What statements show now is what you are getting. For example, someone who has worked in private and public sector jobs and who has years they weren’t paying into Social Security might now be eligible. Or consider this hypothetical example of a public schoolteacher who is married to someone pulling Social Security benefits and receives a pension. According to Zip Recruiter, a retired teacher in the U.S. as of February 2025, who contributed 5% of their salary out of each paycheck to the pension fund, has an average retirement benefit of $42,285 per year, or $3,523 per month, in addition to the approximately $1,976 per month from social security – nearly $5,500 per month combined. Keep in mind this is a hypothetical example, and everyone’s numbers are different and personal to their own lives and financial decisions. Previously, depending on a variety of factors, a percentage of your social security amount, the $1,976 in the example, would be deducted. That is not the case anymore. The example below goes into more detail.

To give you some context, originally, before the passing of the Social Security Fairness Act, the Government Pension Offset (GPO) reduced Social Security benefits by two-thirds for some people. If you had received a monthly civil service pension of $3,523, two-thirds of that, or $2,348 would be deducted from the Social Security benefits. Therefore, if you are eligible for a $2,400 spouse’s or surviving spouse’s benefit from Social Security, you’d get $52 a month (2,400-2,348) along with the civil service pension. The deduction no longer applies.

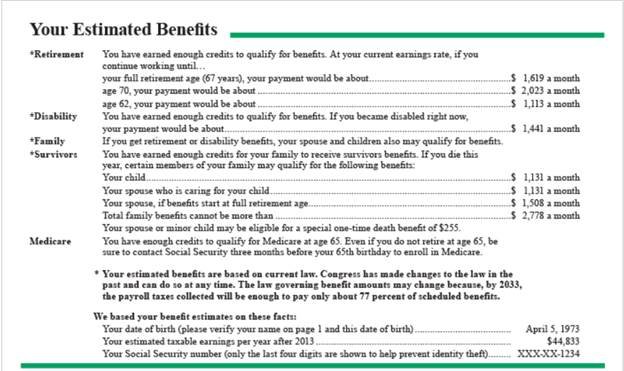

Here is an example of a Social Security benefits statement per Social Security Administration’s website

When can people expect the increased payouts?

The increased payouts will begin this year. In addition, more than 2 million Americans could potentially receive a lump sum payment of thousands of dollars to cover the shortfall in the benefits they should have received in 2024.

Discuss any questions or concerns with a financial professional

Higher payments each month don’t necessarily mean that you now have more money to spend frivolously. The extra funds in your bank account could be used toward working to pay down debt, invested for financial independence in retirement, or managing generational wealth or charitable giving wishes. Consider scheduling an appointment with a financial professional to discuss options you can pursue, that may benefit you in the short- and long-term and align with your financial goals.

Investment advice offered through HighPoint Advisor Group, LLC, a registered investment advisor. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendation for any individual. Although general strategies and / or opinions are revealed, this post is not intended to, nor does it represent or reflect, transactions or activity specific to any one account. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results. All data and information are gathered from sources believed to be reliable and is not warranted to be correct, complete, or accurate.

Investments carry the risk of loss including loss of principal. Past performance is never a guarantee of future results. Vantage Financial Partners Limited is not a tax advisor. Please consult a tax professional for any specific questions regarding your tax situation.

Important Disclosures:

Content in this material is for educational and general information only and not intended to provide specific advice or recommendations for any individual.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

This article was prepared by LPL Marketing Solutions

LPL Tracking #699533

[i] H.R.82 – 118th Congress (2023-2024): Social Security Fairness Act of 2023 | Congress.gov | Library of Congress

[ii] Social Security Explained: How It Works and Types of Benefits

[vi] Delayed Retirement | Born in 1960 | SSA

[vii] Benefits Planner: Retirement | Receiving Benefits While Working | SSA

[viii] Social Security Fairness Act: Windfall Elimination Provision (WEP) and Government Pension Offset (GPO) update | SSA

[ix] Social Security Fairness Act Adds an Average $360 Benefit for Some: Will You Be Getting a Bigger Social Security Check?

[x] Social Security Fairness Act becomes law – IAFF

[xi] Social Security Fairness Act: Windfall Elimination Provision (WEP) and Government Pension Offset (GPO) update | SSA

[xii] Social Security Fairness Act: Windfall Elimination Provision (WEP) and Government Pension Offset (GPO) update | SSA

[xiii] Topic no. 751, Social Security and Medicare withholding rates | Internal Revenue Service

[xiv] Understanding the Benefits

[xvi] Understanding the Benefits

[xvii] my Social Security | SSA

[xviii] Apply for Social Security Benefits | SSA

[xix] The United States Social Security Administration | SSA

[xx] Salary: Retired Teacher in Tennessee (February, 2025)

[xxi] Government Pension Offset

[xxii] The Social Security Statement: Background, Implementation, and Recent Developments

[xxiii] The Social Security Fairness Act: Social Security Benefits Are Changing in 2025